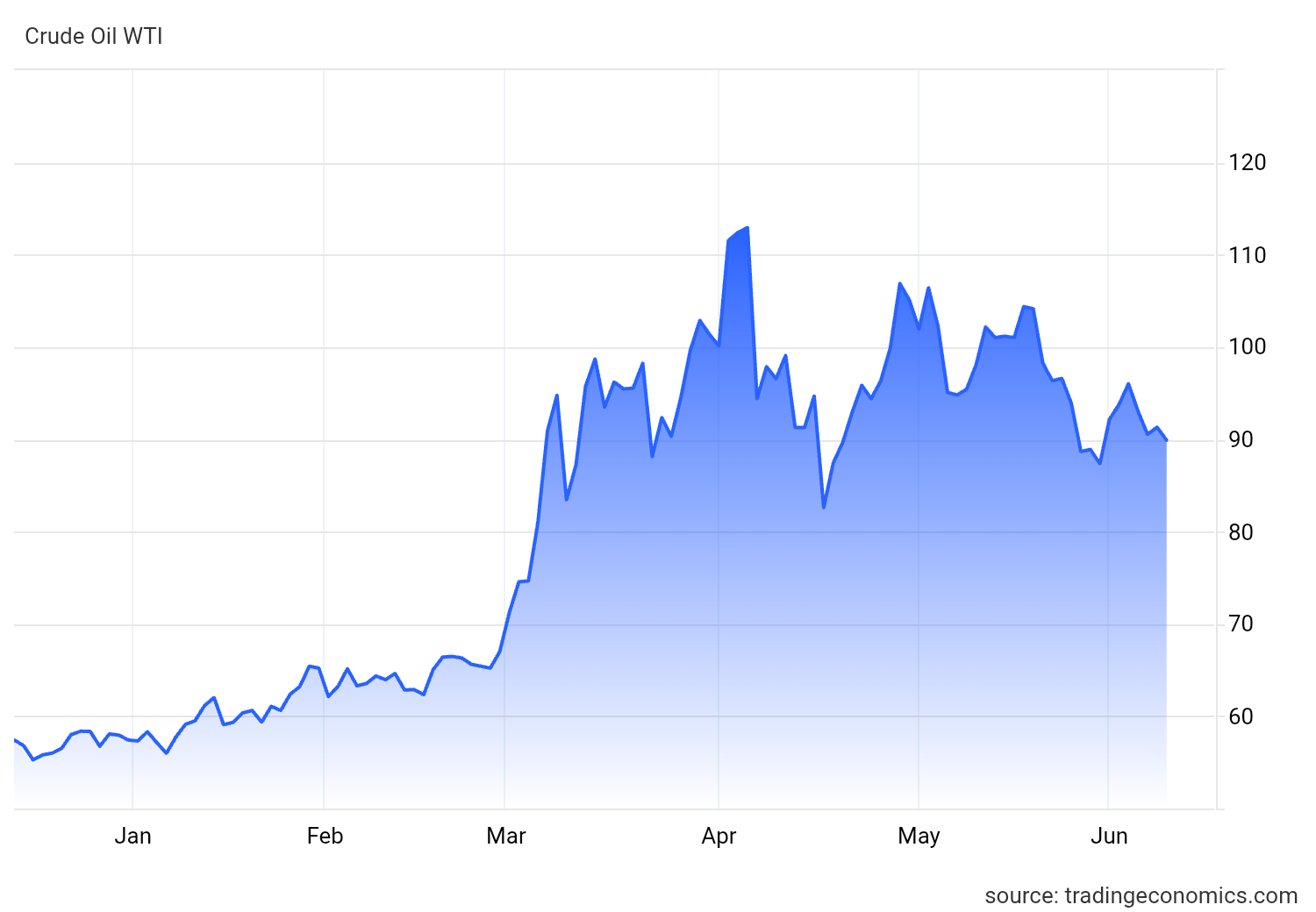

Global oil prices pulled back on Tuesday, June 9, 2026, as news of a temporary ceasefire between Iran and Israel reduced the geopolitical risk premium that had been propping up crude benchmarks. West Texas Intermediate dropped over one percent intraday to trade near $88.75 per barrel, extending a sharp retreat from the mid-$93.00s seen earlier in the week. Brent crude followed, hovering between $93.50 and $94.10 per barrel as traders unwound some of their risk positions.

The selloff reflects a market recalibrating quickly to shifting headlines. When geopolitical tension drives oil prices up, any sign of de-escalation tends to trigger equally fast moves in the opposite direction. That is exactly what happened this week, though the underlying risks that pushed prices higher in the first place have not gone away.

Why the Ceasefire Has Not Ended the Risk

Iran has made clear that the halt in direct attacks is conditional. Tehran warned it could resume hostilities if Israel continues military operations in Lebanon, while disputes over Iran’s nuclear programme and access to the Strait of Hormuz remain unresolved. The strait handles nearly 21 percent of global oil trade, making any threat to its stability immediately relevant to energy markets worldwide.

Traders are not treating this ceasefire as a resolution. They are treating it as a pause, which is why Brent and WTI have pulled back but have not collapsed. The geopolitical risk premium has shrunk, not disappeared.

What the Charts Are Saying

From a technical standpoint, WTI carries a bearish bias. The price is trading below the 200-period simple moving average at $95.25 on the four-hour chart, a level that now acts as resistance rather than support. The MACD remains below zero, pointing to continued downside momentum, while the RSI sitting at 42 signals weak demand without yet reaching oversold territory.

Read also:Kenya Oil Export 2026 at Risk After Sh9.84 Billion Budget Cut

Immediate support for WTI sits at $86.50 to $86.00. A clean break below that level would expose prices to sub-$81.00, close to the swing low seen in April. Brent has already fallen roughly 10 percent over the past month, though it remains nearly 40 percent higher year on year, a reminder of just how much the market has moved over the past twelve months.

OPEC+ and Russia Adding to the Picture

OPEC+ approved a modest production quota increase of around 188,000 barrels per day from July 2026, a signal of stability rather than an aggressive push to flood the market with supply. The group appears to be threading a careful path between supporting prices and avoiding the kind of supply squeeze that draws political pressure from consuming nations.

Russia is tightening the market from a different angle. Refinery disruptions and drone attacks on energy infrastructure have cut Russian crude exports, removing supply at a time when the global market is already sensitive to any reduction. That tightening effect has helped put a floor under prices despite the bearish pressure from the ceasefire news.

What to Watch in the Coming Days

Oil market participants are focused on a short list of developments that will determine whether prices stabilise, recover, or push lower through the rest of June.

Progress or breakdown in the Iran-Israel ceasefire talks is the most immediate variable. Any resumption of direct hostilities would push the risk premium back into prices quickly. Equally, a more durable agreement could see further downside for both benchmarks.

Russia’s export volumes will be watched closely given the supply tightening effect they have had. Further disruptions would support prices. Any recovery in Russian exports would add downside pressure alongside the ceasefire dynamics.

For Kenya and other oil-importing African nations, these price movements carry direct consequences. EPRA’s monthly fuel price reviews are directly influenced by global crude benchmarks, meaning what happens in the Strait of Hormuz and the OPEC+ meeting rooms eventually shows up at petrol stations in Nairobi, Mombasa, and Kisumu.